A high credit score may help you access various financial opportunities by lowering your interest rates and increasing the likelihood that any loan you apply for will be accepted.

Your credit limit — the maximum amount you may borrow using each credit card and other credit accounts — is a significant factor in determining your credit score.

It could be time to request greater credit card limits to raise your total credit limit. Your credit score will appreciate it.

If you wish to expand your ability to make purchases, you may want to consider applying for a higher credit limit, payday loans online Ontario, or other types of loans.

However, you should only do this if you can make the required minimum monthly payments or the whole sum. Here are some suggestions for raising your credit limit.

How Do Credit Limits Work?

The maximum balance you may have on your credit card at any moment without incurring fees or having your transactions rejected has a limit.

The kind of credit card you’re using, your income, and your credit score are just a few variables that affect your credit limit. Your most recent statement should show your credit limit if you need clarification.

Which Credit Limit is Good?

It’s crucial to remember that there isn’t one “good” credit card limit for everyone. For every person, a varied credit limit is ideal.

Low limits are prudent for those with little prior credit card use. Higher limits, although sometimes alluring, are not recommended for cardholders who may be enticed to spend more than they can afford, leading to skyrocketing credit card debt.

A manageable credit limit is a decent credit limit. You may even ask your credit card company to decrease your limit if you believe a high credit limit makes it difficult for you to avoid using it.

Benefits of an Increased Credit Limit

Financial Emergencies

Credit does not simply appear overnight. Finding credit may be challenging, particularly when you need it the most. You’ll be happy you have the cash buffer if you encounter an emergency.

While it’s generally always a good idea to have three to six months’ worth of living costs put aside as an emergency fund, there are rare situations when you may need credit.

For instance, your credit card might come in handy if you’re traveling and have a financial emergency. You’ll be grateful that you have access to this additional credit.

Improved Credit Score

Your credit usage ratio will decrease due to higher credit card limits, which is one of the factors used to determine your credit score.

Simply put, credit utilization refers to how much of your available credit you are currently utilizing. A lower ratio yields better outcomes.

To safeguard your credit score keep the amount on each account below roughly 65% of the credit limit.

Maximum Rewards

The capacity to optimize rewards and cashback is another advantage of having a greater credit limit (provided you carry that type of card).

With an increased credit limit, you may use your card for larger purchases, optimizing your cash back and incentives to save and earn more.

Are You Seeking More Credit?

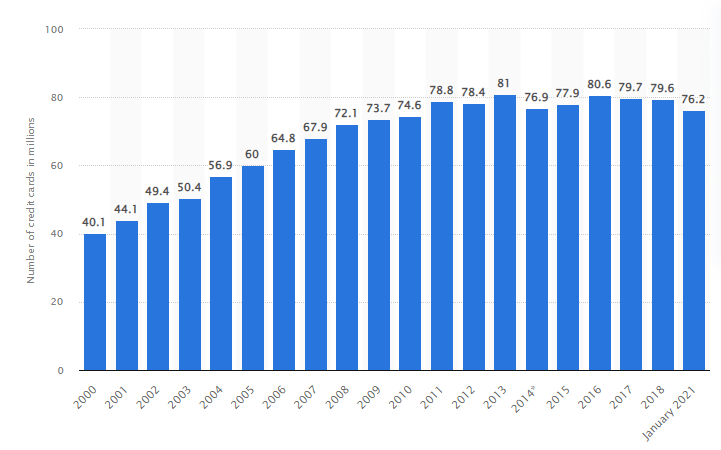

Since 2016, fewer credit cards have been in use in Canada, yet there needs to be a clear explanation for why this is happening.

Many Canadians possess one or two credit cards, according to Statista, making Canada the nation with the most significant credit card penetration in the world.

Number of credit cards in circulation in Canada from 2000 to 2021

Recognize the hazards, including the temptation of having a larger credit limit. With more credit, it’s simple to spend more, and before long, you can be in over your head in debt.

Additionally, a request to increase a credit card’s limit may cause a “hard inquiry” on your credit. A lender’s hard inquiry might lower your credit score and remain on your credit record for years.

Additionally, if your income has decreased, you may postpone your request for a higher limit.

You should wait until you have a reliable, larger salary because your card issuer won’t likely say yes.

Expanding your total credit might improve your credit score if you know how to utilize credit properly. Verify that you comprehend if a larger limit is appropriate for your circumstances.

How to Raise Your Credit Limit?

There are two methods to raise your credit limit. One involves requesting an increase in the credit limit on an active credit card, often one you’ve had for at least a few months.

The credit card provider may check one or more of your credit reports when you submit this request to assess your application.

Depending on the creditor’s policy, this may be a “soft inquiry,” which does not affect credit scores, or a “hard inquiry,” which might have an effect.

If you’re considering asking for a credit limit increase, you should contact the credit card provider to learn more about their policies.

When considering your request, the creditor could need evidence of your yearly income, work status, and regular rent or mortgage payments.

To ensure there are no details that might enhance your chances of being denied for the credit limit increase, you should also examine your credit reports before submitting the request.

The second possibility is that your credit card provider will raise your credit limit on its initiative.

This usually happens when you’ve shown good credit practices, such as paying your bills on time and paying more than the minimum amount due.

Making a new credit card application is another technique to increase your spending power.

The overall amount of money you may access will rise if you have a second card, even if it has the same credit limit as your primary card.

Think about acquiring a credit card with a rewards system or one that provides a sign-up bonus. Choosing your credit card more wisely might help you get rewards for your purchases.

Conclusion

As you can see, increasing your credit limit is simple and has both advantages and disadvantages. You now know how to get a big credit limit if you need one.

{kind=link}